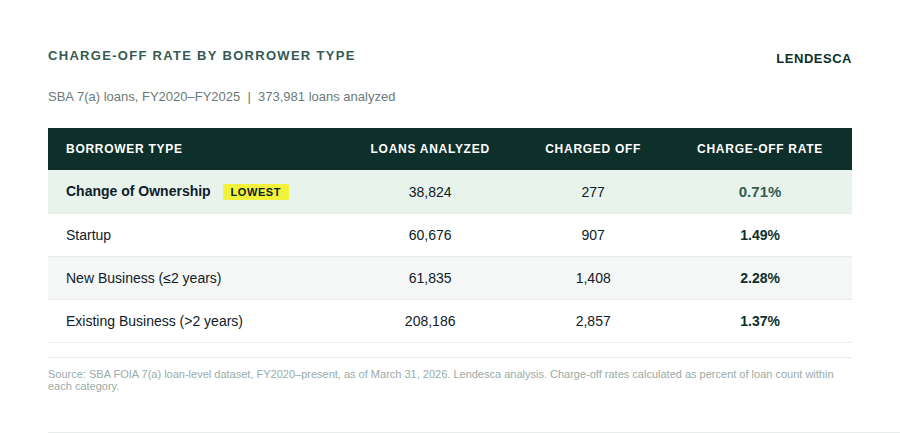

Ask most SBA lenders which loan type carries the least risk and you’ll get a range of answers — usually built on intuition, experience, or anecdote. The data from 373,981 SBA 7(a) loans funded between FY2020 and FY2025 gives a more definitive answer: change-of-ownership loans, used to buy an existing business, have the lowest charge-off rate of any major borrower category in the program. And it isn’t particularly close.

The Numbers

Across all business age categories in the dataset, acquisition loans stand apart:

A charge-off rate of 0.71% means that out of every 1,000 SBA loans used to buy an existing business, only 7 were ever charged off — meaning the SBA determined no further principal or interest would be recovered. That compares to 15 per 1,000 for startups and 23 per 1,000 for businesses two years old or younger.

Out of every 1,000 SBA loans to buy an existing business, only 7 were charged off. That’s less than a third of the rate for new businesses.

It is worth being precise about the distinction between charge-off rates and default rates. The SBA reports a broader default rate — which includes loans in active liquidation and loans purchased but not yet charged off — that runs higher than the figures above. Charge-off is a more conservative measure: it captures only loans that have completed the full loss cycle, after collateral liquidation and Treasury recovery efforts have been exhausted. The charge-off rate is, if anything, the harder standard to clear.

Why Acquisition Loans Perform

The performance advantage of acquisition loans is not a statistical artifact. It reflects the fundamental difference in what a lender is underwriting.

When a borrower applies for an SBA loan to buy an existing business, the lender has access to years of actual operating history — tax returns, cash flow statements, customer records, employee tenure, supplier relationships. The business being purchased has already demonstrated it can generate revenue, cover its costs, and survive the inevitable disruptions that come with operating in the real world. The underwriting question is not “will this work?” but “can this buyer maintain what’s already working?”

Compare that to a startup loan, where the lender is underwriting a projection. The business plan may be well-researched. The borrower may be experienced. But there is no operating history, no proven customer base, no demonstrated cash flow. The SBA guarantee exists in part because that risk profile is genuinely higher — and the charge-off data confirms it.

There is also a collateral dimension. Acquisition loans at the sizes common in the SBA market — the average in this dataset is $1,121,005 — are frequently secured by the hard assets of the business being purchased: real property, equipment, inventory, and the goodwill value of an established brand. That collateral depth gives lenders meaningful recovery options when deals do go wrong, which contributes to the lower ultimate charge-off rate even among loans that experience payment stress.

Size Still Matters Within Acquisitions

Even within the acquisition category, the loan size pattern we identified in our broader charge-off analysis holds. Larger acquisition loans perform better than smaller ones:

- Under $150K: 1.21% charge-off rate

- $150K–$350K: 1.09%

- $350K–$500K: 0.83%

- $500K–$1M: 0.59%

- $1M–$2M: 0.44%

- $2M–$5M: 0.46%

The very small acquisition loans — under $150K — carry a 1.21% charge-off rate, nearly double the overall category average. These tend to be smaller, less-established businesses with thinner margins and less collateral. The sweet spot in terms of credit quality sits in the $500K–$2M range, where charge-off rates drop below 0.60% and the deals are large enough to involve businesses with real operating substance.

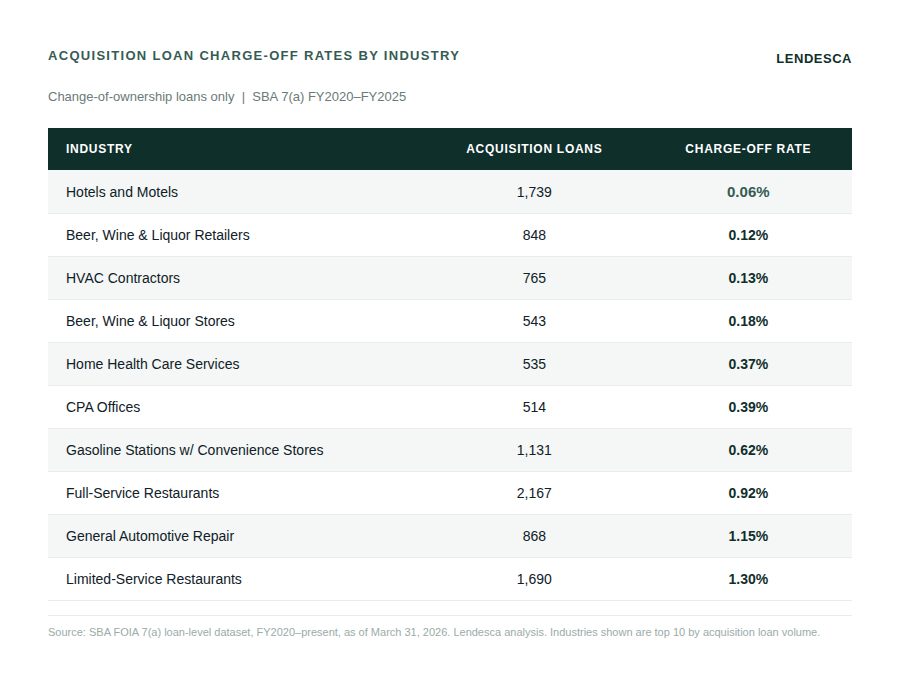

Industry Mix: Where Acquisition Lending Is Cleanest

Not all acquisition loans perform equally. Industry plays a meaningful role, and the data shows clear leaders:

Hotels stand out as the cleanest segment in the acquisition dataset — 1,739 loans with a 0.06% charge-off rate. The combination of hard asset collateral (real property), SBA’s familiarity with hospitality underwriting, and the established nature of the businesses being acquired all contribute. HVAC contractors, liquor retailers, and healthcare services similarly show very low charge-off rates, reflecting the durable demand and collateral profiles of those businesses.

Restaurants tell a more nuanced story. Full-service restaurants show a 0.92% charge-off rate on 2,167 acquisition loans — above the category average but still well below the startup rate for the same industry. Limited-service restaurants run at 1.30%. These businesses carry more risk than, say, a professional services firm, but even in the most challenging food service categories, buying an existing operation with an established customer base outperforms starting from scratch.

The Volume Story: An Underutilized Program

Despite their performance advantage, acquisition loans represent only 10.4% of all SBA 7(a) volume in the FY2020–FY2025 dataset — 38,824 loans out of 373,981. That means 9 out of 10 SBA borrowers are doing something other than buying an established business, and the majority are accepting significantly higher charge-off risk in the process.

The volume of capital deployed, however, reflects the deal sizes involved. Over $43 billion in SBA loans went to business acquisitions during this period, with an average loan size of $1,121,005. These are not marginal transactions. They represent the transfer of real, operating businesses — often from retiring owners to the next generation of operators — with substantial capital behind each deal.

The demographic tailwind here is significant. Baby boomer business owners are transferring their businesses at an accelerating rate, and SBA financing is frequently the most practical mechanism for buyers who lack the capital for all-cash transactions. The acquisition loan category is likely to grow as a share of overall 7(a) volume in the coming years — and if it does, the program’s overall credit performance will likely improve along with it.

What Lenders Should Take From This

The acquisition loan data makes a specific case for lenders building or evaluating their SBA programs.

First, change-of-ownership transactions represent the best risk-adjusted opportunity in the 7(a) program. The charge-off rate is the lowest of any major category, the average loan size is the largest, and the secondary market execution on well-underwritten acquisition loans is strong. If you are going to be in SBA lending, acquisition financing should be a core focus — not an occasional exception.

Second, industry selection within acquisitions matters. Hotels, professional services, healthcare-adjacent businesses, and essential services with real property collateral consistently outperform restaurants and retail. That’s not a reason to avoid restaurants entirely — they represent the highest volume in the acquisition category — but it is a reason to underwrite them with appropriate scrutiny and collateral requirements.

Third, loan size within acquisitions correlates with quality. The sub-$150K acquisition loan is a different credit than a $1.5M acquisition loan. Both may be appropriate, but they carry meaningfully different risk profiles and should be evaluated accordingly.

At Lendesca, acquisition financing is one of our core specialties. We’ve structured hundreds of change-of-ownership transactions across industries and deal sizes, and the performance data above is consistent with what we see in our own portfolio. If you’re a bank looking to build or deepen your acquisition lending capability, we’d welcome the conversation.

Data source: SBA FOIA 7(a) loan-level dataset, FY2020–present, as of March 31, 2026. Analysis covers 373,981 total loans; 38,824 classified as Change of Ownership. Charge-off rates are calculated as a percent of loan count within each category. FY2024 and FY2025 charge-off rates are understated due to insufficient loan seasoning. All figures represent Lendesca’s own analysis of publicly available SBA data.